Ask a founder to name their investor's biggest contribution and most will say the check. Ask them six months later, after the round has been spent and the hard part of building has set in, and the answer often changes. The thing they remember is the introduction — the one warm email that put them in front of the customer, the hire, or the follow-on investor they couldn't have reached on their own.

That's not a coincidence. A fund's real leverage over a portfolio company is rarely the capital alone. It's access. The problem is that access has always been invisible and un-searchable, and so it gets used by accident instead of on purpose.

Why the network stays hidden

Every person at a fund carries a network in their head and their inbox — hundreds or thousands of people they know well enough to vouch for. Multiply that across every partner, every operator, and every other company the fund backs, and the combined graph is enormous. It is also, in most firms, completely illegible.

When a founder needs to reach a specific person, the search happens by memory and luck. They ask their lead partner, who asks around, who maybe remembers someone. Most of the graph never gets queried because no one knows it's there. The intro that would have taken one warm email doesn't happen, and the founder sends a cold one instead — at a fraction of the response rate.

What changes when the graph becomes legible

The shift is simple to describe and surprisingly large in effect: make the combined network searchable, and rank the paths by how strongly each connector actually knows the target.

And "searchable" never means "exposed." Every person and every company on the graph keeps complete control over privacy and sharing — each one defines their own settings for what they share and who can see it. Investors and advisors can even join as external members without connecting an inbox, so the network becomes legible without anyone giving up ownership of their relationships.

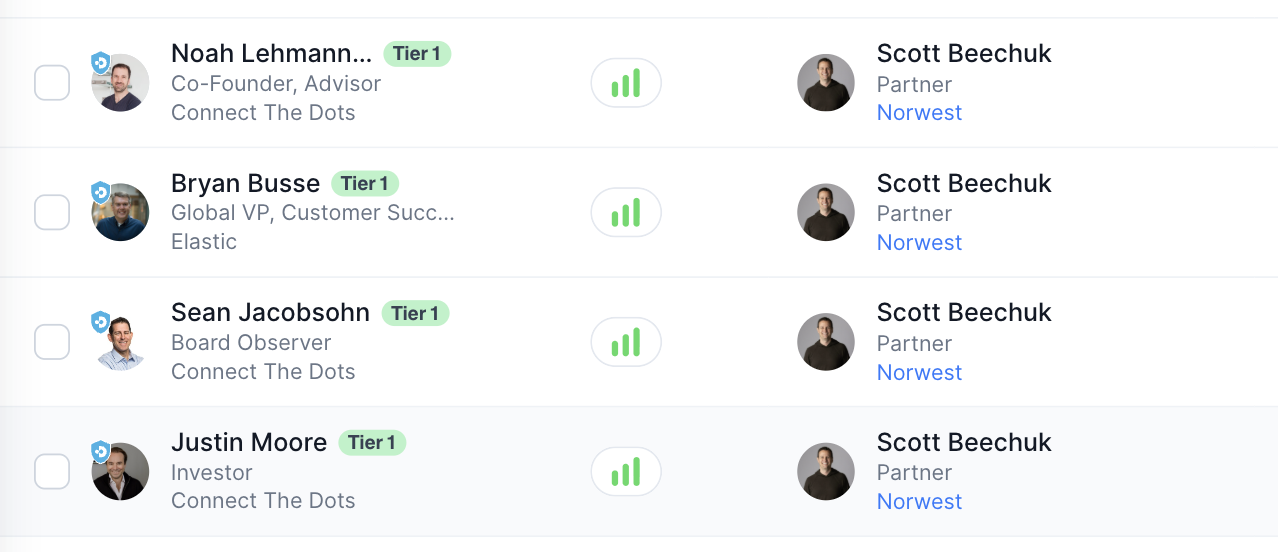

A founder needs to reach a VP of Engineering at a target account. Instead of guessing, they search the fund's whole network — their investors plus every other portfolio company that investor backs — and see the strongest paths to that person, scored by real relationship strength rather than a mutual-connection count. They pick the best one and ask for a single, specific introduction. It lands, because it came through someone the target actually trusts.

The mechanics matter here. Not every connection is worth the same. A path through someone who worked alongside the target for three years is worth far more than a path through someone who traded business cards once. Scoring relationship strength — rather than treating all connections as equal — is what turns a big messy graph into a short, usable list of the intros most likely to work.

The part that surprised us

We expected this to be a productivity win: fewer dead-end Slack messages, more intros made. It was that. But the more interesting effect was on the relationship between founders and their investors.

When access becomes measurable, it becomes a deliverable. A fund can see which of its portfolio companies need which doors opened, and open them deliberately instead of reactively — the board meeting becomes the obvious place to line those intros up. Founders stop treating their investor's network as a favor to be rationed and start treating it as infrastructure they can build on. The value a fund provides shifts from "we wrote a check" to "we can put you in the room" — and both sides can finally see it happening.

That's the motion we've watched work firsthand, and it's why we think the next decade of the founder-investor relationship gets rebuilt around access, not just capital. It's the same idea behind relationship intelligence for VC & PE: your firm's and your portfolio's networks, combined into one searchable graph that turns quiet connections into warm introductions.